Blog

Stablecoins: The Most Important Emerging Market (EM) Financial Innovation You’re Not Pricing In

Tanner Taddeo

Mar 2, 2026

This article was published on Tellimer’s Insight platform, a research destination trusted by financial institutions, development finance organizations, sovereign agencies and policymakers operating across more than 170 emerging and frontier markets.

Tellimer’s audience comprises investment professionals, government agencies, multilateral institutions and strategic decision-makers who rely on forward-looking analysis to assess risk, allocate capital, and shape economic policy across developing economies. This piece was written specifically for that readership to frame stablecoins not as a speculative crypto narrative, but as a structural financial infrastructure shift with direct implications for cross-border trade, liquidity access, monetary influence and the evolving role of the U.S. dollar in emerging markets.

In the article below, we examine how stablecoins are already reshaping settlement dynamics, treasury management and capital access in EM corridors, and why policymakers and market participants alike should factor this innovation into their forward-looking models.

———————————————————————————————

Stablecoins: the most important EM financial innovation you’re not pricing in

Efficient cross-border trade: reducing the cost and risk of cross-border payments in EMs, bypassing correspondent banking networks and expensive FX conversion.

Avoiding parallel and volatile currencies: allowing diaspora to remit, and donor governments and NGO’s to commit and recover hard currency equivalent value to and from countries with volatile currencies, capital controls or fragile banking systems.

The USD will dominate, for now: unlike crypto stablecoins should rely on controlled “on and off ramps” and be underpinned by “real world assets” (RWA), mainly USD.

This special report is written by Tanner Taddeo, CEO of Stable Sea. Tanner founded Stable Sea to modernise cross-border payments and global treasury operations using stablecoin infrastructure. His work centres on bridging traditional financial systems with emerging digital rails to improve efficiency and scale in global commerce. Tanner began his career in humanitarian finance, deploying grant capital in conflict-affected regions and researching technology-driven financial access across Asia and Africa. Tanner holds a Master’s degree in Social Innovation from the University of Cambridge and has worked across investment banking, payments infrastructure and digital assets, including roles at ModusBox, Plaid and Block’s TBD, where he focused on real-time payments and decentralized identity.

“The future has arrived. It is just not yet evenly distributed.” Said the science fiction writer William Gibson. That is true of tokenized finance, and the shift is already underway.

What are Stablecoins?

A stablecoin is a tokenized version of a RWA – typically a US dollar - that is placed on a blockchain. The majority of stablecoins are stablecoins as JP Morgan puts it are “...backed 1:1 by a reserve of fiat currency held by the issuer, to ensure that the stablecoin can be redeemed for its pegged value.”

Given stablecoins are utilized on a blockchain, and a blockchain operates 24/7/265, the utility of stablecoins are found in their instant settlement capabilities, their ability to have logic govern their movements ie “programmability”, and their cost effectiveness, though converting back to local fiat still is expensive.

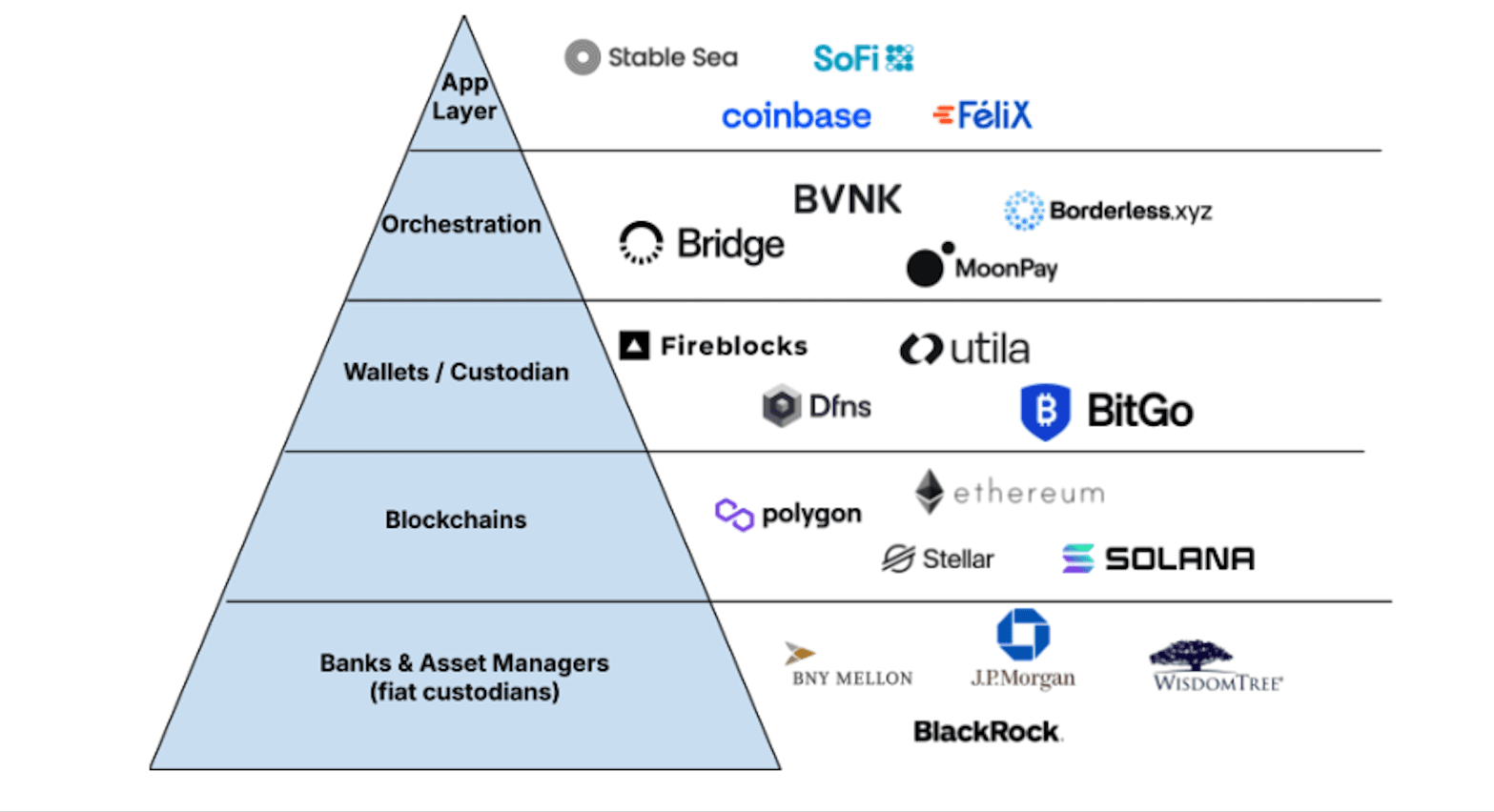

Below is a list of key players in the stack:

Why Stablecoins matter

Stablecoins are already being used today across cross-border payments and particularly in emerging markets, where they are addressing long-standing frictions in settlement, liquidity, and access to U.S. dollars. The growing role of tokenized real-world assets raises the prospect of 24/7 settlement and on-chain liquidity, with the downstream advantages for treasury management, trade finance, and capital efficiency. There are also broader implications for regulation, global financial rails, including how the distribution of stablecoins and tokenized assets could reshape payments, risk, and influence in international trade corridors.

Use Cases for Stablecoins

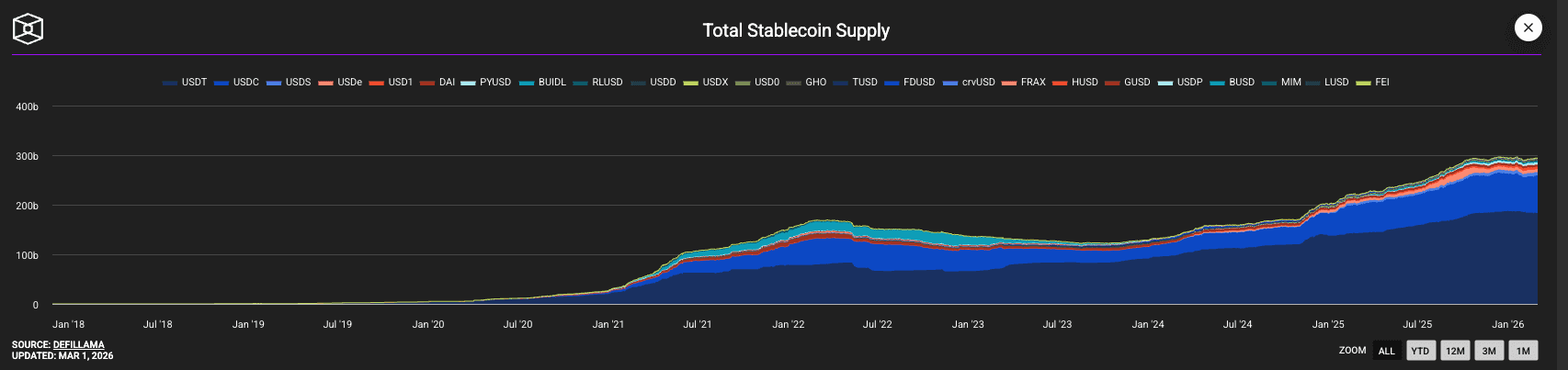

Stablecoin market cap

Let’s start with stablecoins. Since 2018, we’ve seen exponential growth amassing to a total stablecoin market cap of around $300B with three predominant use cases.

Use case 1: Trading

The primary use case for stablecoins was originally to ensure that trading and brokerage firms could quickly get into and out of US dollar denominated positions for trading.

Use case 2: Savings & hedging against currency volatility

Then in the early 2020’s the second use case put stablecoins on the map – providing consumers and businesses in emerging markets with access to the US dollar to hold and hedge against their currency’s volatility. Tether dominated and quickly found distribution through regional exchanges and country-specific FinTechs looking to offer their users access to USD. Tether currently has an outstanding supply/market cap of ~$185B.

Use case 3: Cross-border payments

Circa 2022-2023, the third use case started to take off – the use of stablecoins for cross-border payments. The industry saw the rise of cross-border FinTechs like Conduit, Felix Pago, Bridge, and more.

The “stablecoin sandwich” as it is known, is where a consumer or business sends a FinTech local fiat, the FinTech converts that to USDC/T, sends that stablecoin on-chain to an FX provider, and the FX provider converts USDC/T to local fiat and pays out the recipient in local fiat currency. This model’s value proposition is not necessarily in the cost, rather it’s in the settlement time. To send money abroad, especially to emerging economies can take days, and in some cases, weeks, depending on transaction size and the country in question.

This model has started to take payments market share away from banks and traditional FinTechs that relied on SWIFT.

Interestingly a few fact patterns are emerging here:

Usage concentration. Around 66% of all stablecoin supply is held by consumers or businesses in emerging markets.

Regional volume vs GDP.

Global shifts in regulation

More than 50 countries have implemented stablecoin and/or digital asset regulation

The trendlines are here. Stablecoins are here to stay, and their utility is country-specific.

Stablecoins are the “gateway” digital asset for legitimate finance

Proprietary data from Stable Sea (a leading stablecoin treasury-management platform), suggests that stablecoins are proving to be the ‘gateway to digital assets.’ Many businesses start with stablecoins for cross-border payments, and because most do not trade every day, or over weekends, the next logical question they ask is “what else can I do with my stablecoins?”

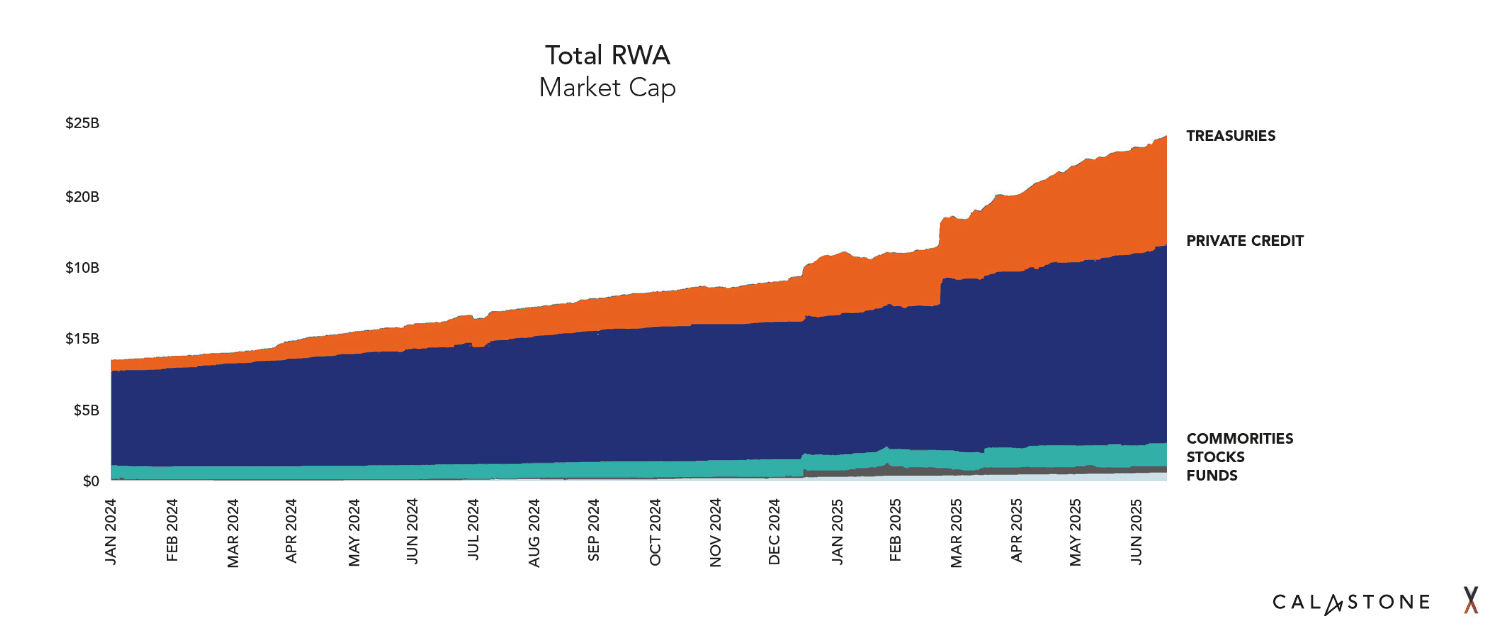

The growth in tokenized assets (colloquially referred to as real-world assets, “RWAs”) has offered a 4th use case for stablecoins – on-chain access to tokenized capital markets products for yield generation.

WisdomTree, Blackrock, Franklin Templton, Fidelity, and more are tokenizing their money markets, fixed income products, and private credit facilities.

The rapid acceleration between 2024 and 2026 was fueled by more than just hype. It was driven by structural utility:

The "Yield Gap": As traditional interest rates rose, "stablecoin" holders (which typically earn 0% yield) sought to move their capital into TMMFs to earn 4–5% risk-free returns while staying on-chain.

24/7 Instant Settlement: Unlike traditional money market funds that settle in T+1 or T+2 days, tokenized funds offer instant settlement, and allow for yield to accrue daily and payout daily. This allows institutions to move millions in liquidity on weekends or holidays.

Collateral Transformation: By 2025, TMMFs moved from being "passive investments" to "active collateral." Major platforms like Crypto.com and Deribit now accept BUIDL tokens as margin for trading, effectively making the fund's yield "stackable" with other strategies

Impact on the USD as the hard currency of EM

This is the early innings of the tokenized revolution, but with history as our guide, it is clear that whichever country, and its private institutions, win in the distribution of stablecoins and tokenized assets, they will create a dependency on the underlying currency and the underlying capital markets securities – and thereby a moat for their currency and subsequent FinTech products.

As with the rise of the current global monetary order and the reliance on SWIFT, these systems are prone to being wielded as tools in geopolitical soft and hard power.

The US dollar has been the global reserve currency since the world went off the gold standard in the 1970s. The rise and adoption of US denominated stablecoins have further entrenched the US dollars’ global position even in spite of the value of the dollar and the bond market whipsawing about. However, Xi Jinping of China has recently called for the renminbi to become the world’s global reserve currency, and while it has publicly turned its back on the idea of a state-controlled stablecoin, it has been putting its efforts into the proliferation and adoption of the digital yuan.

Setting aside how governments can/could use these new tools, one thing remains clear – offering best-in-class financial services to consumers and businesses around the world should result in greater household and business savings on their idle cash and lower the cost of their payments around the world.

The future has arrived, but it’s incumbent upon us in the financial services sector to ensure they become evenly distributed around the globe.